Table of Content

USDA mortgage insurance rates are lower than those for conventional or FHA loans. Thanks to this government guarantee, lenders can offer 100% financing and below-market interest rates without taking on too much risk. Other mortgage programs, like the FHA loan and conventional loan, can have rates around 0.5%-0.75% higher than USDA rates on average. Getting a USDA loan doesn’t necessarily mean your rate will be “below-market” or match the USDA loan rates advertised. Compared to other home loan programs, USDA mortgage interest rates are some of the lowest available.

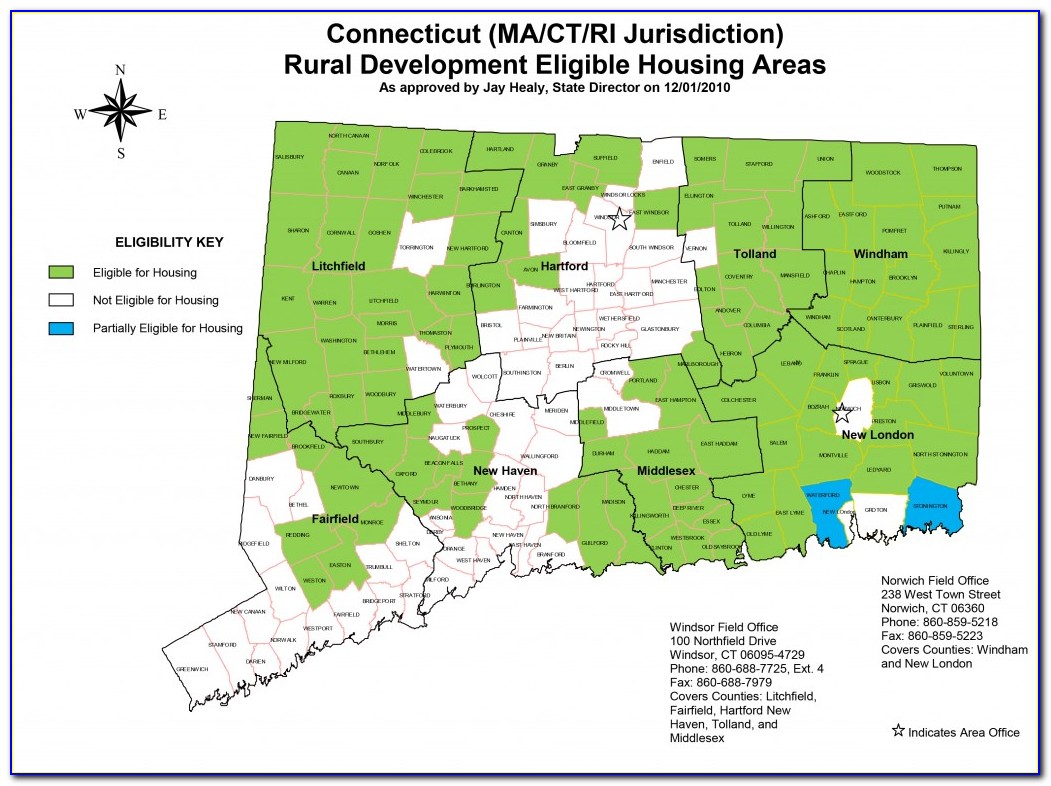

In fact, you might be surprised at just how much of the country is actually eligible for these loans. You can use this USDA eligibility map to find USDA-eligible homes in your area. Look up the address you’re interested in purchasing to verify it falls within a rural area, as determined by the U.S. Buyers who aren’t ready to commit to a specific property or realtor can use USDA’s website to answer most property-related questions and learn more about what the USDA funds can be used for. Also listed are approved lenders that can determine an interested applicant’s eligibility. A number of factors are considered when determining an applicant’s eligibility for Single Family Direct Home Loans.

Cuttler Rd New Caney Texas 77357

Any land outside the shaded areas on the map is fair game. Packagers are encouraged to routinely visit the Direct Loan Application Packagers page for information and resources specific to packaging single-family housing direct loans. While you won’t have a down payment, you will still need to have money available to pay for closing costs. However; USDA allows the seller to contribute up to 6% towards closing costs.

Because closing costs vary, be sure to shop around to find the most suitable combination of low mortgage rates and low costs. The USDA sets no loan limits, but the amount you can borrow is limited by your income and your household’s debt-to-income ratio. The USDA typically caps debt-to-income ratios to 41 percent. However, the program may be more lenient for borrowers with a credit score over 660 and stable employment, or who show a demonstrated ability to save. With the USDA Rural Housing Program, your home must be located in a rural area. Many small towns meet the rural eligibility requirements of the agency, as do suburbs and exurbs of many major U.S. cities.

Allow for Low Credit Scores

Seller concessions may include all or part of a purchase’s state and local government fees, lender costs, title charges, and any number of home and pest inspections. USDA loan rates are often lower than conventional 30-year fixed mortgage rates. This means a USDA loan is often more affordable overall than a comparable FHA or conventional loan. Many USDA-approved lenders don’t even list the USDA loan on their loan application menu. So if you think you’re eligible for a zero-down USDA loan, it’s worth asking your shortlist of lenders whether they offer this program.

For example, if the median salary in your city is $65,000 per year, you could qualify for a USDA loan with a salary of $74,750 or less. The application process for a USDA mortgage works just like any other home loan. You’ll compare rates and choose a lender, complete an application , provide financial documents, wait for the lender’s approval, and then set a closing day. Although the USDA backs this program, it typically isn’t the one lending money.

Type of Property You Want

They also have lower interest rates than many other loan programs, and their guarantee fee — the USDA’s approach to mortgage insurance — is cheaper than on other mortgages as well. USDA improves rural community economic health by working with private lenders to guarantee loans to borrowers for the construction of rural multi-family housing units and individual homes. The USDA Rural Development loan is meant to help moderate to low-income families get access to housing and mortgage loans in some of the less densely populated parts of the country. By enabling homeownership, the USDA helps create stable communities for households of all sizes. Once you’ve used the USDA loan map to determine if a property is eligible, your next step is to confirm you meet income requirements. The amount you can earn to have access to USDA loans is limited and varies by location and household size, so use this tool for more specific guidance.

Every effort is made to provide accurate and complete information regarding eligible and ineligible areas on this website, based on Rural Development rural area requirements. Rural Development, however, does not guarantee the accuracy, or completeness of any information, product, process, or determination provided by this system. Final determination of property eligibility must be made by Rural Development upon receipt of a complete application.

Farm Loans

You also need to shop around with a few different USDA mortgage lenders. Each USDA lender sets rates differently — so comparing personalized offers from more than one company is the only way to find your lowest option. To obtain a direct USDA loan, you have to show that you can’t get a loan from another lender. You also will have to show that you don’t have access to any other housing that’s safe, clean or otherwise fit for life. In general, though, both the direct and guaranteed USDA loans are only available for certain types of properties.

Eligible applicants for the persistent poverty and SECD set-aside funds must demonstrate that 100% of the benefits of an approved grant will assist beneficiaries in the designated areas. USDA is making this funding available under the Rural Business Development Grant program to support business opportunities or business enterprise projects in rural communities. Eligible entities are rural towns, communities, state agencies, authorities, nonprofits, federally recognized tribes, public institutions of higher education, and non-profit cooperatives. Individual and for-profit businesses are not eligible for this grant. As you can see, there’s a lot that goes into determining a city’s (and a property’s) USDA eligibility. To see eligible areas in your region, simply search a local address on the USDA property eligibility map.

The data relating to real estate for sale on this web site comes in part from the Internet Data exchange (“IDX”) program of the San Antonio Board of Realtors. Real estate listings held by brokerage firms other than USDA homes team, are indicated by detailed information about them such as the name of the listing firms. More information on FAR can be found at the USDA Economic Research Service FAR web page. All projects located 100% within territories or possessions of the United States eligible to apply under ReConnect, are eligible to request up to $35,000,000 in 100% grant funds.

If you have less than two years in a job, however, you may not be able to use your bonus income for qualification purposes. The USDA Rural Housing loan is available as a 30-year fixed-rate mortgage only. There is no 15-year fixed option, or adjustable-rate mortgage program available via the USDA. The U.S. Department of Agriculture’s website maintains a list of approved lenders for the Rural Housing Program.

Property eligibility areas can change annually and are based on population size and other factors. This map is a helpful guide, but the USDA will make a final determination about property eligibility once there's a complete loan application. When it comes to USDA homes, you should be more focused on property eligibility instead of area eligibility. Most of the United States is eligible for a USDA home loan. USDA mortgage interest rates are among the lowest on the market, next to VA loans.

But in fact, 97% of the U.S. map is eligible for USDA loans, including many suburban areas near major cities. Any area with a population of 20,000 or less can be an eligible rural area. The only exception is for very-low-income borrowers, who may qualify for a USDA Direct home loan. In this case, you’d go straight to the Department of Agriculture to apply rather than to a private lender.

The USDA Rural Development loan is among the most accepting in regards to credit history. FHA requires a FICO score of 640 and some conventional programs accept nothing less than 740, but USDA will approve applicants with scores as low as 620, which is well below national average. Negative credit events like foreclosures, short sales, and bankruptcies are not immediately disqualifying for USDA loans. Approved lenders are encouraged to look past individual credit events to consider the applicant’s overall credit worthiness. A current, positive credit portfolio with no recent late payments or collection accounts may qualify an applicant for a mortgage. Eligible properties must be located within USDA-defined rural areas.

No comments:

Post a Comment